Bank of England Quarterly Credit Union Statistics Q2/24

Thursday 19 December 2024

Introduction:

The Bank of England gathers information from credit unions’ quarterly reports to create a statistical report about the credit union sector in the UK. However, submitting and processing the returns data takes around six months, which delays the publication of the data.

This briefing is based on the data collected by the Bank of England and shows the statistics for the second quarter of 2024 for credit unions in Great Britain. Below are the headline statistics for the British credit union sector and graphs that display the sector’s trends over the past five years (Q2/19-Q2/24)

It is important to note that this data represents all credit unions that submitted their regulatory returns for the financial quarter. There may be significant differences in financial trends experienced by individual credit unions that are not represented in this data. Furthermore, some credit unions may have submitted their annual returns late, and so the last quarterly data may be slightly inaccurate.

KEY STATISTIC FOR THE BRITISH CREDIT UNION SECTOR FOR THE SECOND QUARTER (Q2) of 2024

Credit unions (returns submitted): 232

Total Members (including juniors): 1,561,295

Total Assets: £2.73 Billion

Total Shares: £2.35 Billion

Total Capital: £336 million

Total Loans: £1.83 billion

Quarterly Income: £72 million

Quarterly Expenditure: £69.1 million

Quarterly Profit/Loss: +£3.2 million

Trends in the British Credit over the Last Five Years:

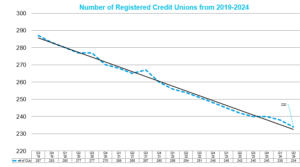

The second quarter of 2024 saw 232 credit unions submit their returns to the PRA. This is a decline of two credit unions from the previous quarter. There is a continued trend of slight decline in the number of credit unions in Great Britain, shown in the trend line below. During this reporting period there was one credit union who entered administration, Castle and Crystal. There are multiple reasons for the continued decline in number such as the increased rate of credit unions merging.

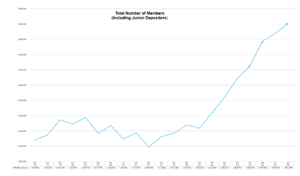

Total Number of Credit Union Members.

There has been an increase in Great Britain’s total members, to their highest point of 1,561,295 members (including juvenile depositors). This is an increase of 0.88% from the previous quarter and an increase of 4.87% from the prior year.

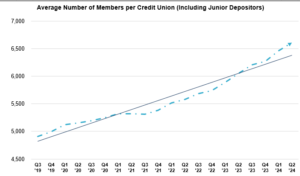

Average Number of Members per Credit Union:

The graph demonstrates that there has been a steady increase in the average number of members per credit union. This was calculated by dividing the number of members by the number of credit unions. It is important to note that credit unions do vary a lot in terms of membership size. However, this is more to visualise the growth of membership as a sector. This is the equivalence of 116 news members per credit union on average, a 1.75% increase from the previous quarter.

The average membership is 6,730

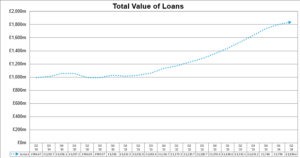

Total Value of Loans:

The total value of credit union loans in Great Britain increased by 2.23% from Q1/24 to Q2/24, rising from £1.79 billion to £1.83 billion, an increase of around £40 million. Continuing pressure of the cost-of-living, energy price cap increases from January 2025, can be partly attributed to the ongoing demand for credit. Furthermore, with an increasing number of members in credit unions, the total value of loans is more likely to increase.

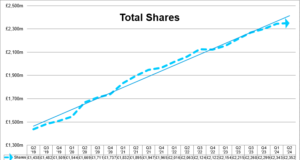

Total Shares:

Total credit union shares also demonstrate that membership savings grew 0.27% from the previous quarter, with a 6.09% growth from the previous year. The total share value in Q2/24 £2.35 billion.

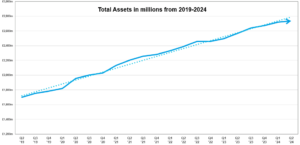

Total Assets:

Total assets experienced a 0.61% quarterly growth, marking around 6.55% increase from the previous year. In the second quarter, the assets amounted to £2.73 billion, representing a £14.79 million increase from the previous quarter.

Loan to Asset Ratio

The total loans to asset ratio for Great British Credit Unions has increased to 67.27% from 66.2% in the previous quarter. This means that credit unions are issuing more loans compared to the growth in their assets. It could be indicative of a higher demand for loans from members or a strategic decision by the credit unions to increase their lending activities.

Total Income, Expenditure, and Profit.

In the second quarter of 2024, British credit unions recorded a total surplus of £3.2 million, marking a -28% change in profit from the previous quarter. However, when comparing Q2/2024 to Q1/2024, the following changes were observed across the sector.

- Total income increased by 7.6% (£72.3 million from £67.2 million)

- Total Expenditure increased by 10.1% (£69.1 million from £62.7 million)

Total Arrears

During Q1 2024 – Q2 2024, the total value of net liabilities in arrears increased by 10.24%, which was a smaller increase compared to the previous quarters. By Q2 2024, the total arrears reached £172.8 million. The graph shows a consistent rise in arrears over the past five years. This reflects the ongoing financial difficulties faced by many households, forcing them to borrow to manage the escalating cost of living.

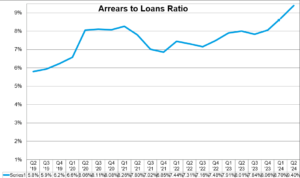

Arrears to Loans Ratio:

The arrears-to-loan ratio demonstrates how much is in arrears in the loans given out (repayment has been missed on one or more occasions). In Q2/24, the arrears-to-loans ratio was 9.39%. This has increased by 0.69% from the previous quarter to 10.08%.

Total Capital

The total capital increased to £336.3 million in the second quarter of 2024, representing a 2.24% increase. An increase in capital is important for credit unions because it enhances their financial stability and their capacity to support their members’ financial needs. With higher capital, credit unions can better absorb unexpected losses, continue operations during economic downturns, and expand their lending activities. Additionally, a stronger capital position can improve the confidence of regulators, members, and potential investors in the credit union’s financial soundness.

Capital to Asset Ratio:

This ratio indicates the extent to which a credit union’s operations are funded by its own capital rather than debt. A higher capital-to-asset ratio suggests a stronger financial position and a greater ability to absorb losses without jeopardising solvency. The capital-to-asset ratio increased from 12.1% to 12.3% in Q1/24 to Q2/24. The recent increase in the capital-to-asset ratio is a positive sign of credit unions’ financial health.

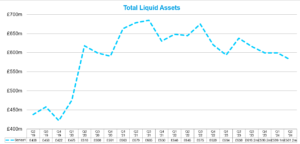

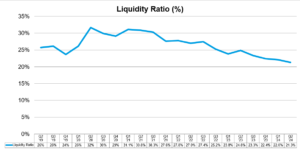

Liquidity:

The total liquid assets for the British sector for Q2 2024 was £581.1 million, a decrease from £604.5 million. The ratio decreased from 22% to 21.3% from Q1/24 to Q2/24.

Credit unions need to carefully manage their liquidity to ensure they can meet member demands and obligations. Assessing their expenditures, lending strategies, and overall financial performance may be beneficial to address the decrease in liquidity and make necessary adjustments.

Summary:

The second quarter of 2024 saw 232 credit unions in Great Britain, with a total of 1,561,295 members. The total assets amounted to £2.73 billion, with total shares at £2.35 billion and total loans at £1.79 billion. The quarterly income was £72 million, with a profit of £3.2 million. Over the last five years, there has been a slight decline in the number of credit unions, while the total number of credit union members has been increasing. The average number of members per credit union also rose.