Consumer Duty

Wednesday 25 February 2026

Update 13/03/2026 – Consumer Duty Good and Poor Practice Examples to Improve consumer understanding of financial products and services

The FCA have published good and poor practice examples of consumer understanding of financial products and services under the consumer duty. The update highlights key findings ,areas for improvement with smaller firm specific examples.

The FCA’s consumer understanding: good practice and areas for improvement webpage can be accessed here

Update 25/02/2026 FCA Consumer Duty Work Update:

The FCA have recently updated examples of good and poor practice on Duty Board Reports.

- The FCA this year also plan to include extra insight for smaller firms in any new good and poor practice materials, as well as expanding existing Duty best practice resources

- create sector-specific guides to help small firms apply outcomes-based regulation, starting with a pilot for credit broking firms this year.

ABCUL will be advocating for a credit union sector-specific guide in conversations with the FCA.

Refreshed Webpages:

The FCA have also refreshed the Consumer Duty webpages to make them easier for firms, particularly smaller firms, to find the information most relevant to them. The refreshed pages bring key guidance, including good and poor practice examples, into a clearer, more structured layout, helping firms navigate the FCA’s expectations more quickly and with greater confidence.

The FCA also welcomes feedback on the refreshed duty pages by email: consumerduty@fca.org.uk

Feel free to reach out to the Advocacy team at advocacy@abcul.org if you prefer for ABCUL to pass on feedback to the FCA on the refreshed duty pages.

Update 27/02/2025 – Removal of requirement for Consumer Duty Board Champion

The Consumer Duty is the FCA’s new regulatory regime for consumer care. It requires financial services firms to proactively ensure they are delivering good outcomes for consumers. This information guide will detail the requirements for credit unions put in place by the new Consumer Duty.

The Consumer Duty is centered on the new Consumer Principle, that states firms must act to deliver good outcomes for retail customers. The Consumer Duty expects a higher standard of conduct for credit unions than previous conduct rules, by requiring them to proactively and consistently ensure they deliver good outcomes for customers. The Duty should be embedded across a credit union’s business, from product governance to the delivery of member support services.

The Consumer Duty will come into force on the 31st July 2023, by which time credit unions will need to ensure that its products and services are meeting the consumer duty regulations.

To implement the Duty, credit unions will need to assess their current processes and identify any areas that need improvement to better align with the FCA’s requirements. This may involve making changes to existing policies and procedures, as well as developing new ones. For example, credit unions may need to review the way they provide support to or communicate information about products to members to ensure they meet the higher standards placed by the Duty. In addition, credit unions must train staff and volunteers on the Consumer Duty and how to deliver the Duty day-to-day.

Beyond the implementation deadline, the Duty will require credit unions to regularly monitor and evaluate the outcomes being received by members to remain compliant with the Duty’s requirements. It will also require an annual report to be approved by the board, that demonstrates the credit unions compliance with the Duty.

For any questions on implementing the Consumer Duty, please contact advocacy@abcul.org.

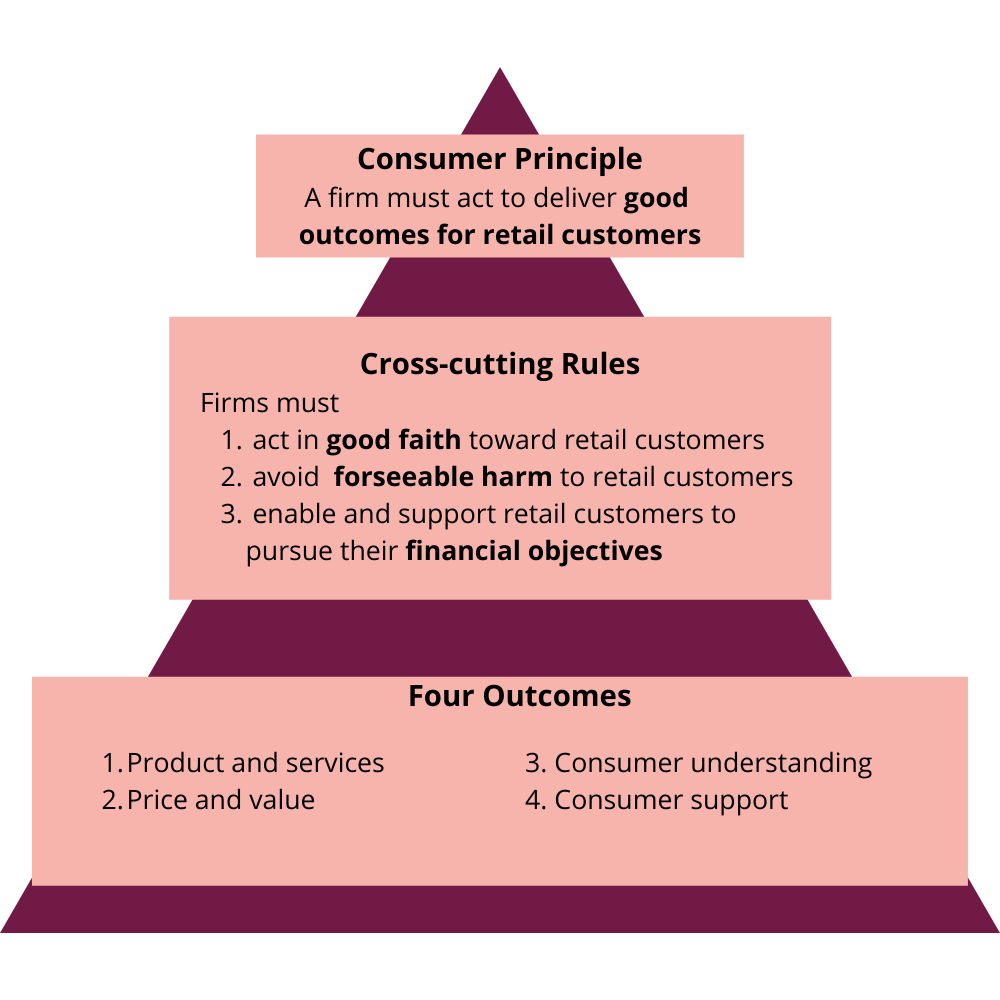

Structure of the Consumer Duty

The Consumer Duty has three levels of rules in how it applies to firms, as shown in the diagram below. The central principle of the duty is the Consumer Principle that requires firms to deliver good outcomes for retail customers. Supporting the consumer principle there is the three cross-cutting rules, which set the general standard of conduct required from firms in meeting the Consumer Duty. The third level to the Consumer Duty is the four consumer outcomes, which identify the areas of the design and delivery of products and services where firms are required to deliver good outcomes.

Consumer Principle: The primary rule at the centre of the Duty is the Consumer Principle (Principle 12). This rule states that “Firms must act to deliver good outcomes for retail customers” and for firms to place their consumers’ interests at the heart of their activities.

Principle 12 imposes a higher standard than both FCA conduct principles that credit unions are already required to meet – Principle 6 (a firm must pay due regard to the interests of its customers and treat them fairly) and Principle 7( A firm must pay due regard to the information needs of its clients and communicate information to them in a way which is clear, fair and not misleading).

Cross-Cutting Obligations: The three cross-cutting rules establish the standards of conduct the FCA expect under Principle 12. The cross-cutting rules require firms to both proactively and reactively:

- Act in good faith towards retail customers

- Avoid causing foreseeable harm to retail customers

- Enable and support retail customers to pursue their financial objectives

Consumer Outcomes: The four consumer outcomes sets out the following areas of the relationship between firms and customers where they must act to deliver good outcomes and meet the cross-cutting rules in practice

- Products and services

- Price and value

- Consumer understanding

- Consumer support

The Conduct Rule: The Consumer Duty adds a new conduct rule, which requires that all credit union conduct rule staff and volunteers will have an obligation to meet the Duty. This new conduct rule 6 states “You must act to deliver good outcomes for retail customers”.

The new conduct rule also applies the three cross-cutting rules of the Duty to individual conduct rule staff and volunteers.

Key Implementation Deadlines

The FCA has set the following deadlines for all firms it regulates for the implementation period of the Duty. The key deadline that credit unions should have regard to is that the Consumer Duty regulations came into force on the 31st July 2023, and credit unions need to ensure that all existing product and services meet the Consumer Duty regulations by this date.

31st October 2022: Credit unions should complete and agree an implementation plan with their board

30th April 2023: Credit unions should aim to complete a review of all existing products and services in scope of the Duty, so they can:

- Share with third parties by the end of April 2023 the information necessary for them to meet their obligations under the Duty

- Identify where changes need to be made to their existing open products and services to meet the Duty and make these adjustments by the end of July 2023

31st July 2023: Consumer Duty regulations come into force for open products and services

31st July 2024: Consumer Duty regulations come into force for closed products and services

An open product is a product open for sale, distribution or renewal to members. A closed product, on the other hand, is a product no longer open for sale or renewal to members, but where there are active and pre-existing contracts in place for that product.

Guidance on Applying and Implementing the Consumer Duty

Application to Credit Union Products and Services

The Consumer Duty applies to FCA regulated activities and their ancillary activities. This section will identify the key credit union products and services that the Consumer Duty applies to.

The Consumer Duty will apply to all credit unions as it applies to deposit-taking (which includes all credit union savings products). Where a credit union offers a wider or more complex range of products, it is likely to have more activities within scope of the Duty.

The tables below give a list of the main credit union products and services that are within scope of the Duty. The Duty will also apply to any credit union activity that is ancillary to a regulated activity. Ancillary activities are unregulated activities necessary for the performance or completion of a regulated activity. For example, the design of a product or service, the production of communications to members and ongoing member support services connected to a regulated activity would be subject to the Duty.

| Product or Service | Guidance Notes |

| Deposit-taking | Deposit-taking is an FCA regulated activity, meaning that any of the below credit union products are subject to Consumer Duty requirements:

· Savings accounts · ISA accounts · Child Trust Funds · Transactional deposit accounts or current accounts · Save-as-you-borrow style loan products (where a savings requirement is built into the loan agreement and payments) Please note that we are waiting for clarification from the FCA on whether credit union attached share loans are within scope of the Consumer Duty regulations. |

| Consumer Credit Activity | Any credit related activity within the scope of consumer credit regulation, i.e. requires a consumer credit license, is also within the scope of the Consumer Duty. Such consumer credit regulated activities a credit union may carry out with permission include:

· Debt counselling · Debt adjustment · Credit information services · Borrower-lender-supplier agreements · Credit cards · Hire purchase and conditional sale agreements (pending reform of the Credit Unions Act 2023) |

| Insurance Distribution | General insurance distribution is an FCA regulated activity, that many credit union will look to offer with the pending changes to the Credit Unions Act in 2023. Credit unions offering general insurance distribution will need to meet the product distributor requirements of the Duty. |

| Issuing E-Money | Issuing e-money is an activity within scope of the Duty, whether issued by a third party card provider or a credit union with permission to issue e-money. Where a credit union offers members a prepaid card account with a third party provider, the credit union would count as a distributor of this product provided to members. |

| Mortgages | Mortgages are an FCA regulated activity and are within scope of the Duty (with the exception of credit union second charge mortgages that have an exemption) |

Any credit union activities that are not a FCA regulated activity, and are not ancillary to an FCA regulated activity, will be outside of scope of the Consumer Duty. For example, the Consumer Duty would not apply to unregulated money and budgeting advice.

Furthermore, credit union borrower-lender agreements benefit from an exemption from Consumer Credit regulation under the Financial Services and Markets Act, and do not qualify as an FCA regulated credit activity. Therefore, the Consumer Duty does not apply to credit union loans that do not require a consumer credit license. The exception to this, noted in the table above, are credit union save-as-you-borrow style loan products, which are brought into scope due to the regulated savings aspect of the loan. Nevertheless, credit unions should aim to meet the Duty in principle with loans and other relevant activities that are exempt. This is both to meet the member-centric spirit of the credit union movement and to maintain support for the exemption from consumer credit regulation that credit unions benefit greatly from.

Third Parties

Where a credit union works with third party firms to provide a product to members, there will be different requirements placed on the credit union and third party depending on their role in delivering that product. For the Consumer Duty, the requirements placed on firms depend on whether they are classified as a manufacturer or distributor of a product. The FCA defines manufacturers and distributors as below:

Manufacturer: a firm which creates, develops, designs, issues, manages, operates, carries out or underwrites a product. There may be more than one firm that manufactures a product (co-manufacturers).

Distributor: a firm which offers, sells, recommends, advises on, arranges, deals, proposes or provides a product.

For many products, credit unions will serve the role of both the manufacturer and distributor, so will need to meet the Duty requirements for both roles. Where the credit unions works with another firm to provide or distribute a product or service, they will need to collaborate and share information with them so both parties can meet their obligations as either a manufacturer or distributor as discussed throughout the guide. It will be raised in the guidance on the four consumer outcomes where there are specific requirements for manufacturers and distributors.

Furthermore, credit unions will also rely on an unregulated third party to deliver many products and services, such as backend software providers, whose actions can have a material impact on members’ outcomes. In these instances, the credit union is responsible for ensuring that the unregulated third party supports good outcomes being delivered under the Duty. Accordingly, a credit union should set expectations/requirements for unregulated third party providers so it can meet its obligations under the Duty.

The Conduct Rule

The new conduct rule means that all credit union conduct rule staff and volunteers will have an obligation to meet the Duty. This new conduct rule 6 states “You must act to deliver good outcomes for retail customers”. This means that the Duty applies at the level of individual staff and volunteers as well at the level of the credit union.

The new conduct rule applies the same obligation as the cross-cutting rules of the Duty, requiring that all conduct rule staff fulfil the following rules:

- You must act in good faith towards retail customers.

- You must avoid causing foreseeable harm to retail customers.

- You must enable and support retail customers to pursue their financial objectives.

Here conduct rule staff may cause foreseeable harm by both act and omission, so should be trained by the credit union to proactively prevent foreseeable harm. Conduct rule staff and volunteers should also be equipped to take account of the target market of a product and any characteristics of vulnerability of members.

These obligation apply to all conduct rule staff and volunteers regardless of whether they have a direct relationship with members, and requires them to consider how their actions may affect the interests and outcomes of members. However, expectations place on a conduct rule staff or volunteer will depend on the scope of their role in the credit union, as well as factors such as their seniority and level of experience.

In instances where conduct Rule 4 (you must pay due regard to the interests of customers and treat them fairly) would apply, the requirements are replaced by the Duty’s higher standard. Where a credit union’s activity is outside of the scope of the Duty (e.g. lending that is outside of the Duty), this activity is still subject to Rule 4 requirements.

Non-Prescriptive Application

The Duty presents a move to outcomes–based regulation and is non-prescriptive. This means that the Duty does not set out how credit unions should deliver good outcomes on the ground, and that credit unions will need to establish how it delivers good outcomes based on the products it offers and needs of the credit union’s membership. However, credit unions will need to engage with the substantive content of the Consumer Duty regulations, as explained in this guide, to understand the principles and requirements for delivering good outcomes.

Reasonable Application

The FCA applies a concept of ‘reasonableness’ as to what it expects from different firms implementing the Duty. What is considered as ‘reasonable’ when implementing the Duty depends on the nature of the firm, the product and the relationship with its customers.

Acting reasonably to deliver outcomes does not require credit unions to take on a fiduciary duty or provide an advisory service where it does not already exist.

In general, the actions required of credit unions to meet the Duty will be proportionate to the risk of harm to members, e.g. where a member falls into arrears there will be a higher level of action required from credit unions than promoting an easy access savings account to members.

Non-Retrospective Application

The Duty does not apply retrospectively, i.e. it does not apply to the credit union’s conduct prior to the implementation deadline of 31st July 2023. However, existing products and services need to be reviewed and amended to meet the Duty by this deadline.

Furthermore, the Duty and its requirement to correct for any potential risks of harm to customers does not interfere with the vested rights a firm has under pre-existing contracts. Therefore, where a contract has been entered into before the Duty comes into force (before the end of July 2023), the Duty will not interfere with nor require credit union to update the terms of the contract. The terms include any payments, fees or charges that the credit union has a right to as part of the contract.

Vulnerability

The Consumer Duty places an emphasis on firms actively considering and tailoring services towards customers with vulnerability. As will be highlighted in the explanation of the four consumer outcomes, specific and proactive consideration of vulnerability is built in throughout the Consumer Duty regulations.

To meet the requirements of the Duty, credit unions should look to train and assist frontline staff/volunteers to understand how to actively identify information that could indicate vulnerability and, where relevant, seek information from members with characteristics of vulnerability that will allow staff to respond to their needs. Credit unions should also look to set up systems and processes for member services in a way that supports and enables vulnerable members to disclose their needs.

Cross-cutting Rules

The three Consumer Duty cross-cutting obligations set out the overarching conduct the FCA expects how firms should act to deliver good outcomes for retail customers. There are three cross-cutting rules:

- Firms must act in good faith towards retail customers.

- Firms must avoid causing foreseeable harm to retail customers.

- Firms must enable and support retail customers to pursue their financial objectives.

The cross-cutting obligations apply at all stages of the member’s interaction with a product/service. The cross-cutting rules apply at the level of the target market (for example during the design of a product, making pricing decisions or designing communications for that product), but also for each interaction with an individual member.

These rules require that products need to be regularly reviewed, and the impact of any changes to products should be considered. Meeting the cross-cutting rules require all firms, including credit unions, to react both proactively and reactively to meet these principles.

It should also be noted that the cross-cutting obligations also apply through the new conduct rule for credit union staff and volunteers.

As part of meeting these obligations, credit unions should consider the impacts of the following factors on a member’s needs and decisions:

- Cognitive and behavioural biases

- Characteristics of vulnerability

- Asymmetry of knowledge between the credit union and the member

Act in good faith

The first cross-cutting rule requires that firms “must act in good faith towards retail customers”.

Good faith is defined for the Consumer Duty as a “standard of conduct characterised by honesty, fair and open dealing and acting consistently with the reasonable expectations of retail customers”.

The FCA provides the following examples of where it would not consider a firm to act in good faith:

- Failing to take account of customers’ interests, for example in the way it designs a product or presents information

- Seeking inappropriately to manipulate or exploit customers, for example by manipulating or exploiting their emotions or behavioural biases to mis-lead or create a demand for a product

- Taking advantage of a customer or their circumstances, for example any characteristics of vulnerability, in a manner which is likely to cause detriment

- Carrying out the same activity to a higher standard or more quickly when it benefits the firm than when it benefits the customer, without objective justification

Acting in good faith does not mean that a credit union needs to act in a fiduciary capacity where it is not already required to do so.

According to the Consumer Duty, acting in good faith towards members requires that where the credit union has identified that a member has suffered foreseeable harm as a result of an act or omission of the credit union, it must act in good faith and take appropriate action to rectify the situation, such as providing redress to the member in some cases. This requirement does not apply where the harm was causes by a risk inherent to the product, provided the credit union reasonably belies that the member understood and accepted that risk.

Avoid causing foreseeable harm

The second cross-cutting rule requires that firms “must avoid causing foreseeable harm to retail customers”. The rule requires credit unions to work proactively to avoid causing foreseeable harm through its conduct, products and services.

Avoiding causing foreseeable harm to members does not mean a credit union has a responsibility to prevent all harm. To assess if a harm is foreseeable, a credit union must consider what the credit union is reasonably expected to have predicted or known when providing a product or service, and what is within the credit union’s control. A product may have inherent risks which members accept by selecting that product, that are not prevented by this cross-cutting rule. However, the credit union will be held responsible for ensuring that the member understood and accepted these risks that are inherent to the product.

The following are examples of foreseeable harm:

- Members with characteristics of vulnerability being unable to access and use a product or service properly because the customer support is not accessible to them

- Members being unable to exit a product or service, where the current service isn’t right for them anymore, because the credit union’s processes are unclear, onerous or difficult to navigate

- Products and services causing harm because the credit union used an inappropriate distribution strategy, which leads to products and services being distributed widely to individual for whom the products were not designed and whose interests they do not serve

- Products and services performing poorly where the credit union had not taken adequate steps to consider how members would be affected

The FCA considers that foreseeable harm may be caused by both an action or omission of a credit union. Credit unions will need to act to avoid causing foreseeable harm to the member throughout the full duration of the product or relationship with that member. Credit unions have a responsibility to prevent foreseeable harm in a direct relationship with a member, but also through its role in a distribution chain where it works with a third party to offer a product to members.

Avoiding causing foreseeable harm to members includes:

- Ensuring all aspects of the design, terms, marketing, sale of and support for products avoid causing foreseeable harm

- Ensuring that no aspect of business unfairly exploits consumer behavioural biases or members’ characteristics of vulnerability

- Identifying the potential for harm that may arise if the credit union withdraws or changes a product

- Responding to emerging trends that create new sources of harm, including trends highlighted in FCA communications

- Taking appropriate action to mitigate the risk of actual or foreseeable harm

Examples of taking appropriate action to mitigate the risk of actual foreseeable harm include:

- Updating or amend the design of the product or the distribution strategy

- Updating information about a product

- Ensuring that members do not face unreasonable barriers, for example when they want to switch products or provider, or when they want to make a complaint

- Where a product is withdrawn, allowing time and support for members to find suitable alternatives

Enable and support retail customers

The third cross-cutting rule states that firms must “enable and support retail customers to pursue their financial objectives”. This places the obligations on credit unions to create an environment where members are enabled and supported to make decisions in their interests. Credit unions will need to consider this obligation at the level of designing a product /service, in producing communications to members, and in delivering members support services.

The extent that a credit union will need to act to support members in reaching their financial objectives depends on the nature of the product provided.. The FCA specifies that for a non-advisory service is being provided to members (such as savings or a consumer credit loan), it can be assumed that the member’s financial objectives are just to purchase, use and enjoy the full benefits of the product. As most credit union services are non-advisory, the expectation under this cross-cutting rule will predominately be for the credit union to support members to access and fully benefit from the use of a produce or service. With services that are discretionary or advisory (such as the regulated consumer credit activity of debt counselling), a credit union could only be expected to know the financial objectives of a member based on the information that has been disclosed to the credit union (as well as any information that must be obtained for that advisory service by law).

Enabling and supporting members to pursue their financial objectives includes acting to enable members to make decisions in their interests, including by:

- Ensuring all aspects of the design, terms, marketing, sale of and support for the credit union’s products meet and do not frustrate the objectives and interest of the member

- Designing products or services with clear and straight-forward features so they can be understood by members in the target market

- Making sure members have the information and support they need, when they need it, and to make and act on informed decisions

- Enabling members to enjoy the use of their product, and to switch or exist the product where they want to without unreasonable barriers or delay

- Considering the characteristics of members that communications are aimed at, and tailoring their communications accordingly so that they are likely to be understood

- Helping members navigate the information the credit union provides, making it easy for members to identify the key information and their available options

- Taking account of members behavioural biases and the impact of characteristics of vulnerability in all aspects of interaction with members

Where a credit union becomes aware of a specific financial objective sought by a member that relates to a product, it should consider how to support progress towards achieving that objective in interactions with the member. However, credit unions are not required to go beyond what is “reasonably expected” by members when enabling and supporting their financial objectives. In addition, this cross-cutting rule does not mean that a credit union needs to provide advice where they are not required or qualified to do so.

This cross-cutting rule may also require the proactive provision of information or offer of support when a credit union declines to provide a product to a member or where an individual is declined membership. In this situation, it may be appropriate to provide information to enable or support that member to achieve their objectives, such as signposting to a debt advice charity where a member is declined for a consumer credit product.

The Four Consumer Outcomes

The four consumer outcomes regulations set out how credit unions should design and deliver products and services to meet the cross-cutting obligations and deliver good outcomes for members. The FCA sets out the four consumers outcomes based on key aspects of the relationship between financial services firms and consumers. These four outcome areas are:

- Products and services

- Price and value

- Consumer understanding

- Consumer support

Credit unions will need to determine how the four outcomes apply to the products, communications and member support services they provide, and review where these services will need to be amended in line with the Duty. Credit unions should also build the delivery of the four outcomes into their relevant policies and procedures.

The steps that credit unions are required to take for the four outcomes is dependent on its role in delivering a product or service. It will be indicated where the requirements under a consumer outcome are different for manufacturer or distributor of a product/service. In many cases, products and services are both manufactured and distributed by the credit union, in which case all the requirements for an outcome will be relevant. Where a credit union works with a third party to deliver a product or service, it must meet the consumer outcome requirements that that apply to its role in manufacturing/distributing the product.

Outcome One: Products and Services

This first consumer outcome is based around ensuring that products and services are fit for purpose. The products and services outcome puts in places a series product governance obligations for credit unions. The requirements for this outcome differ depending on whether the firm manufactures or distributes a product, though credit unions should have regards to both sets of requirements if it holds both roles in the delivery of a product or service.

Manufacturers

The core requirement of the products and services outcome is one of product governance. The Consumer Duty requires that a manufacturers must maintain, operate and review a process for the approval a product, or a significant adaptation of a product, before it is marketed or distributed. This section sets out requirements that apply to credit unions where they are a manufacture of a product or service.

Product Approval Process

For all products that are not a closed product, the Consumer Duty regulations set out that a credit unions undertake a product approval procedure that must:

- Specify the target market for the product at a sufficiently granular level, taking into account the characteristics, risk profile, complexity and nature of the product.

- Take account of any particular additional or different needs, characteristics and objectives that might be relevant for individuals in target market with characteristics of vulnerability

- Ensure that all relevant risks to the target market, including any relevant risks to individuals with characteristics of vulnerability, are assessed

- Ensure that the design of the product:

- Meets the needs, characteristics and objectives of the target market

- Does not adversely affect specific groups of individuals within the target market, including those with characteristics of vulnerability

- Avoids causing foreseeable harm in the target market

- Ensure that the intended distribution strategy is appropriate for the target market

- Require the manufacturer to take all reasonable steps to ensure that the product is distributed to the identified target market

For a closed product, the manufacturer must maintain, operate and review a process to assess and regularly review whether any aspect of the product results in the credit union not complying with the cross-cutting obligations in relation to existing customers. This process must also assess and regularly review whether a closed product affects groups of customers in different ways and in particular whether any members in the target market with characteristics of vulnerability are adversely affected by any aspect of the product.

Review of Products

Manufacturers are required to regularly review products in scope of the Duty, taking into account any event that could materially affect the potential risk to the product’s target market. This review should include an assessment of:

- Whether the product meets the identified needs, characteristics and objectives of the target market, including members with characteristics of vulnerability

- Whether the intended distribution strategy remains appropriate

Where a manufacturer identifies any circumstances related to the product that may adversely affect members, the manufacturer must take appropriate action to mitigate the situation and prevent harm. If appropriate, the manufacturer should inform other firms in the distribution chain on the action taken.

Testing Products

To the extent that it is proportionate and reasonable, a credit union should test their products appropriately, such as by carrying out scenario analysis where relevant. This testing should assess whether the product meets the identified needs, characteristics and objectives of the target market, including any vulnerable members. to assess whether their products are meeting the needs of the identified target market.

If testing shows the product inadequately meets the needs of the target market and/or those with characteristics of vulnerability, they must not bring the product to the market if it is still under development, or halt marketing/distribution if an existing product needs to be amended.

Collaboration for Co-Manufacturers

Where credit unions, work with another firm to co-manufacture a product , they must create a written agreement detailing their respective responsibilities in the product approval process.

Selection of Distribution Channels and Providing Information to Distributors

Manufacturers are required to select distribution channels that are appropriate for the target market. Where working with a third party distributor, they must also provide information to the distributor to enable them to understand the characteristics of the product, the identified target market and the intended distribution strategy for the product.

Distributors

The below requirements set out the requirements of the products and service outcome for credit unions distributing a product.

Distribution Arrangements

A distributor must maintain, operate and review product distribution arrangements to ensure that:

- The product it distributes avoids causing, or where that is not practical, mitigates foreseeable harm

- It ensures the needs, characteristics and objectives of the target market are considered

It is the distributor’s responsibility to obtain information from a third-party manufacturer to understand the characteristics of the product, the identified target market and intended distribution strategy.

Review and Action

A distributor must regularly review its distribution arrangements to ensure that they are up to date and appropriate, and verify that it is only distributing each product to the identified target market.

Where a distributor identifies an issue following a review, it must make appropriate amendments to the distribution arrangements to prevent harm.

Outcome Two: Price and Value

The second consumer outcome requires firms to deliver a fair price and value to their customers for products and services in scope of the Duty. This outcome requires that financial services products provide fair value, where the amount paid for the product is reasonable relative to the benefits of the product.

This section will outline the different obligations under the price and value outcome for credit unions manufacturing and/or distributing a product.

Manufacturers

A product manufacturer must ensure its products provide fair value to the intended target market and carry out a value assessment of its products.

A value assessment must be carried out before a product is marketed to members (except for existing products that need to be assessed before the 2023 implementation deadline). Credit unions should ensure they are considering whether a product will deliver fair value when designing a product. An initial value assessment must also be carried out for any significant adaptations of a product. The credit union should document any value assessments and subsequent reviews it undertakes.

The value assessment must be reviewed at a frequency that is appropriate to the nature and duration of the product. When a manufacturer identifies in reviewing a value assessment that the product no longer provides fair value, it must take appropriate action to mitigate (and potentially remediate) harm caused to existing and new users of that product.

An assessment of whether a product provides fair value must include a consideration of the following:

- The nature of the product, including the benefits that it will provide/may reasonably be expected for it to provide, and the quality of the product. These benefits may include non-financial benefits, such as a high-level of customer service and support for members.

- Any relevant limitations of the product

- The expected total price to be paid by the member throughout the duration of the product. The expected total price includes: the price agreed on entering into the contact for a product, such as repayments; any regular charges or fees payable throughout the duration of the product; any contingent charges (such as dormancy fees, extra administrative charge, late payment fees); and any non-financial costs the retail customer is asked to provide.

- The impact of an characteristics of vulnerability in the target market, that may mean that vulnerable members do not receive fair value from products and services.

A value assessment should also consider the costs of the credit union in manufacturing/distributing the product, as well as the market rate and charges for a comparable product.

Where another firm distributes the product, manufacturers should ensure that the distributor has the necessary information to understand the value provided by that product.

Distributors

A credit union or another firm must ensures its distribution arrangements are consistent with it providing fair value to members, by considering:

- The benefits the product is intended to provide to members

- The characteristics, objectives and needs of the product’s target market

- The interaction between the price paid by the member and the extent or quality of services provided by the distributor

- Whether the impact of the distribution arrangements (including a remuneration for a distributor) would mean the product is no longer of fair value to members

Where the credit union is a product distributor, and it identifies that a product no longer provides fair value, it must take appropriate action to:

- Mitigate the situation and prevent further occurrences of possible harm to members

- Redress any foreseeable harm that has been caused to members as a result of the product distribution arrangements

- Inform relevant third party manufacturers or other distributors about any concerns of harm to members and mitigating actions of the credit union

Where a credit union distributes a product manufactured by another firm, the credit union is responsible as a distributor to take all reasonable steps to ensure the product distributed is of fair value. A distributor is required to consider a manufacturers fair value assessment when determining the distribution strategy for a product.

These requirements for product distributors under the price and value outcome have a specific exemption for/do not apply to the distribution of general insurance products, as these products have specific regulations covering their price and value under the FCA PROD sourcebook that apply to insurance firms.

Outcome Three: Consumer Understanding

The third consumer outcomes requires that firms communications enable consumers to understand their products and service, their features and risks, and the implications of any decisions they must make. This involves credit unions providing members with the information they need, at the right time, and presented in a way they can understand. Specifically, the consumer understanding outcome requires that credit unions support members understanding by ensuring its communications:

- Meet the information needs of members

- Are likely to be understood by members

- Equip members to make decisions that are effective, timely and properly informed

- Are clear, fair and not misleading

This section will detail the requirements placed on credit unions in making sure its communications meet the consumer understanding outcome.

Scope of Application of the Consumer Understanding Outcome

The consumer understanding outcome applies to all firms involved in the production, approval or distribution of communications to retail customers, regardless of whether a direct relationship with a retail customer or not. This means that the consumer understanding rules may apply to regulated third-parties that assist in the production of communications, as well as a credit union.

The consumer understanding rules apply to all communications throughout a firm’s interaction with retail customers (regardless of the medium or channel used to communicate e.g. verbal or via social media) including before, during, and after the sale of a product. The rule also applies to interactions that do not relate to a specific product but are connected to activities in scope of the Duty. For example, where credit unions are at all promoting the fact that they offer savings/deposit-taking, however general the promotion, the Duty would apply. It is also strongly advisable that credit unions follows the principles of the consumer understanding outcome rules in respect of communication related to their loan products that are outside of the scope of the Duty.

Timing of communications

For a credit union to provide information on a timely basis, it must communicate in good time for its members to make effective decisions both before deciding to enter a product and throughout the duration of a product or service.

Selecting the communication channel

When considering the methods of communicating with members/prospective members, credit unions must be satisfied that the communication channel:

- Enables the communication of relevant information that members are likely to need in a way that supports effective decision-making

- Provides an appropriate opportunity for members to review the information, and where relevant, assess their options

Guidance for producing understandable communications

In supporting the understanding of members through its communications, credit unions should:

- Explain or present information in a logical manner

- Use plan and intelligible language and, where use of jargon or technical terms is unavoidable, explain the meaning of any jargon or technical terms as simply as possible.

- Make key information prominent and easy to identify, including by means of headings and layout, display and font attributes of text, and by use of design devices such as tables, bullet points, graphs, graphics, audio-visuals and interactive media;

- Avoid unnecessary disclaimers

- Provide relevant information with an appropriate level of detail, to avoid providing too much information such that it may prevent retail customers from making effective decisions.

Tailoring communications

To support member’s understanding of the credit unions products and services, the credit union must tailor the communications for the intended customer group, taking into account:

- Member’s characteristics, including characteristics of vulnerability

- The complexity of the product

- The communication channels used

For product specific communications, credit unions should consider the target market for that product. For non product-specific communications, a credit unions should consider the characteristics of the general membership and common bond.

One-to-one interactions with members

When interacting with members on a one-to-one basis, such as in-branch, on the phone or other forms of interactive dialogue, a credit union must:

- Tailor the communication to meet the information needs of that member, taking into account if they have characteristics of vulnerability

- Ask the member whether they understand the information and if they have any further questions, particularly where this information is regarded as key information, such as where it prompts a member to make a decision

Testing, monitoring and adapting communications

Credit unions must assess communications before they go out to members to ensure they meet the consumer understanding outcome. If a credit union has the resources available, it should consider testing of key/important communications.

Credit unions should also be regularly monitoring to see the impact communications are having, to be able to identify if communications need to be adapted to deliver good outcomes for members. Credit unions should in particular adapt or amend a communication where it’s identified that there are areas of common misunderstanding amongst members or where members are not experiencing good outcomes, including particular groups of members with characteristics of vulnerability. For example, where a credit union has communicated to members to prompt an action, and there has been a low level of response, it is likely that a communication hasn’t been understood properly.

There is an obligation under the Duty to notify other firms in a distribution chain that have produced a communication that the communication is not delivering good outcomes.

Outcome Four: Consumer Support

The fourth consumer outcome requires that firms provide support that meets their customers needs. This section will set out the requirements for credit unions in meeting the consumer support outcome.

Scope and Application of the Consumer Support Outcome

The consumer support outcome applies directly to all firms that are responsible for interacting directly with and providing support to retail customers.

This outcome applies regardless of the channel used when interacting with or providing support to members, and includes all electronic communications including social media. The rule also applies to interactions/support that does not relate to a specific product but are connected to activities in scope of the Duty, meaning that credit unions will need to apply the outcome across their members support services. It is also strongly advisable that credit unions follows the principles of the consumer support outcome in respect of their loan products that are outside of the scope of the Duty.

Design and Delivery of Customer Support

The Duty requires that credit unions must design and deliver support to their members so that it:

- Meets the needs of members, including those with characteristics of vulnerability

- Ensures that members can use a product/service as reasonably anticipated

- Ensures that it includes appropriate friction in the member journey to mitigate to the risk of harm and gives members sufficient opportunity to understand and assess their options and any risks

- Ensures that members do not face unreasonable barriers (including unreasonable additional costs) during the lifecycle of a product, such as when they want to:

- Make general enquiries or requests to the credit union

- Amend or switch the product

- Transfer to a new product provider

- Access a benefit which the product is intended to provide

- Make a complaint

- Cancel a contract, agreement or arrangement or otherwise stop using a product/service with the credit union

Here unreasonable barriers are defined as those which are likely to cause members unreasonable additional steps to progress their objectives, including steps which are: unreasonably onerous, time-consuming, complex, difficult to understand. It would also be considered as a unreasonable barrier where a member is asked for unnecessary information or evidence. However, this does not prevent there being appropriate friction in a customer journey. Furthermore, unreasonable additional costs here include where a member incurs unreasonable exit fees or other charges, delays, distress or inconvenience.

To meet the consumer support outcome, credit unions should ensure that members do not face unreasonable delays when trying to engage with the credit union. Credit unions should also try to mitigate unreasonable delays to:

- Any payments due to members from when the payment has been agreed

- The credit union requesting necessary information or evidence from members

- The credit union processing information received from members

Monitoring, Oversight and Governance

Monitoring Outcomes

The Consumer Duty requires that credit unions regularly monitor the outcomes that members are experiencing from their products and services. Regular monitoring should be carried out by a credit union to enable it to identify whether there are any risks that they are not meeting the cross-cutting rules or delivering the four consumer outcomes.

The frequency of monitoring and type of information a credit union will collect to effectively monitor the outcomes received by members will depend on the nature of the product/service and the credit unions role in delivering that product/service. However, the Consumer Duty regulations require that a credit union regularly monitors the outcome members receive from: the products the credit union provides to members; the communications the credit union has with members; and the support the credit provides to members.

As well as monitoring broadly whether the credit union is meeting its obligations under the Consumer Duty and cross-cutting rules, the monitoring carried out by a credit union must enable it to determine:

- Whether members are being, or have been, provided with products that have been designed to meet their needs, characteristics and objectives

- Whether the products that members use provide fair value

- Whether members are equipped with the right information to make effective, timely and informed decisions

- Whether members receive the support they need

- Whether certain groups of members are receiving different outcomes compared to another group of members for a certain product

- Whether members have suffered harm as a result of actions/omissions of the credit union

The Consumer Duty requires that a credit union must take action to address the situation where it identifies any instance where there is a risk to it meeting the cross-cutting rules or delivering the four consumer outcomes. Credit unions should also take a appropriate action where it finds that a group of members are receiving worse outcomes than other groups of members for the same product. This requirement does not apply to a bad outcome for a member that relates to risks inherent to that product, that the credit union reasonably believes that the member understood and accepted.

Where a credit union works to distribute a product to members that is manufactured by a third party firm, a credit union may be obliged to share information with the third party firm to support its monitoring of the consumer outcomes.

Sources of data and information credit unions may want to collect and assess as part of monitoring for the Consumer Duty include:

- Member feedback– both formal and informal feedback to help identify trends and areas of improvement

- Complaints– recording the number and content of complaints and where possible, completing a root cause analysis to investigate the cause of the complaint

- Feedback from staff/volunteers – credit unions should enable and encourage staff/volunteers to report on whether good outcomes are being delivered on the ground particularly those in frequent, direct contact with members

- Reviewing processes and policies– to consider their effectiveness in delivering good outcomes for members

- Research via testing or focus groups – where it has the capacity, credit unions may consider undertaking testing on its products, communications and support services to test whether they are supporting/delivering good outcomes

The information gathered through monitoring should be documented for the credit union’s own record, but does not need to be sent to the FCA. The findings of this monitoring and any corrective actions taken to address risk of harm must be summarised in an annual report for the board.

Where the credit union recognises that it has caused foreseeable harm

Where a credit union becomes aware or has identified that a member has experienced harm that was foreseeable, it should investigate the circumstances of foreseeable harm. The Duty requires that firms take corrective action or provide redress to a customer where appropriate. Credit unions are also required to engage with third parties firms involved in providing a product or service where it has been identified that harm has been caused to a member.

Notifying the FCA

Credit unions should note that the Consumer Duty regulations require firms in a distribution chain to notify the FCA if it becomes aware that any other firm in that distribution chain is/may not be complying with Consumer Duty rules.

Whilst credit unions will not be required to submit information gathered via monitoring to the FCA, they should have regard to the general obligation to notify the FCA of any issues that they would reasonably expect notice.

Oversight and Governance

The Consumer Duty regulations require that the Consumer Duty obligations are reflected in a credit union’s strategies, governance, leadership and people policies. The credit union’s board is ultimately responsible for the oversight of the implementation of the Duty, and should ensure that the Duty is put into practice across all aspects of the business. After the implementation period, the board is required to sign off an annual assessment of the credit unions compliance of the Duty, which is discussed further in the section below.

It should also be ensured that the consumer outcomes are a central focus of the credit union’s risk control arrangements under the SYSC section of the FCA Handbook, and the Consumer Duty must also become a central focus of a credit union’s internal audit function.

Updated: 27/02/2025: The FCA confirmed in February 2025 that they no longer expect credit unions and other firms to have a Consumer Duty Champion. Now that they Duty is in full effect the FCA want to give credit unions greater flexibility on their ongoing arrangements and firms are free to retain the role if they wish to do so. All references to “board champion” will be amended in the FCA’s Finalised Guidance on Consumer Duty (FG22/5) in due course.

It is recommended by the FCA that a member of the board is appointed as a ‘Consumer Duty Champion’, to ensure that the Duty is being discussed regularly and raised in all relevant discussions. This would not be a prescribed role under SMCR and does not remove responsibilities from the whole level of the credit union / board for implementing the Duty.

Annual Assessment and Report to the Board

Credit unions will be required to prepare a report to be approved by board at least annually, that sets out the results of its monitoring of the Consumer Duty outcomes.

The board must review and approve a credit union’s report on the outcomes being received by members, confirm whether it is satisfied that the credit union is complying with its obligations under the Duty, and assess whether the credit union’s future business strategy is consistent with its obligations under the Duty.

There is not a set format required for the annual assessment, and a credit union should complete the report in a manner proportionate to the scale and complexity of the credit union. However, the detail of the report should be sufficient to allow the board to assess whether the credit union is meeting its obligations under the Duty.

When approving the report, the board must also agree upon:

- Any action required to address any risks identified by the report that indicates members may not receive good outcomes

- Any action required to address any instance identified where members have not received good outcomes

- Any amendments to the credit union’s business strategy to ensure it remains consistent with meeting the credit unions obligations under the Consumer Duty.

Credit unions are not required to submit the annual report to the FCA. However, the FCA may request to see a credit unions most recent annual assessment for the Consumer Duty. The first report is to be considered by the board within 12 months of the new regulations coming into force (i.e. credit union boards should sign off the first report by 31st July 2024).

Further Information

For further information, the FCA Consumer Duty guidance may be read in conjunction with the amendments to the FCA Handbook. ABCUL has also issued guidance on completing a Consumer Duty implementation plan.