HM Treasury Review of the Financial Ombudsman Service Consultation and FCA/FOS CP25/22: Modernising the Redress System consultation

Wednesday 23 July 2025

HM Treasury: Review of the Financial Ombudsman Service Consultation Members’ Briefing

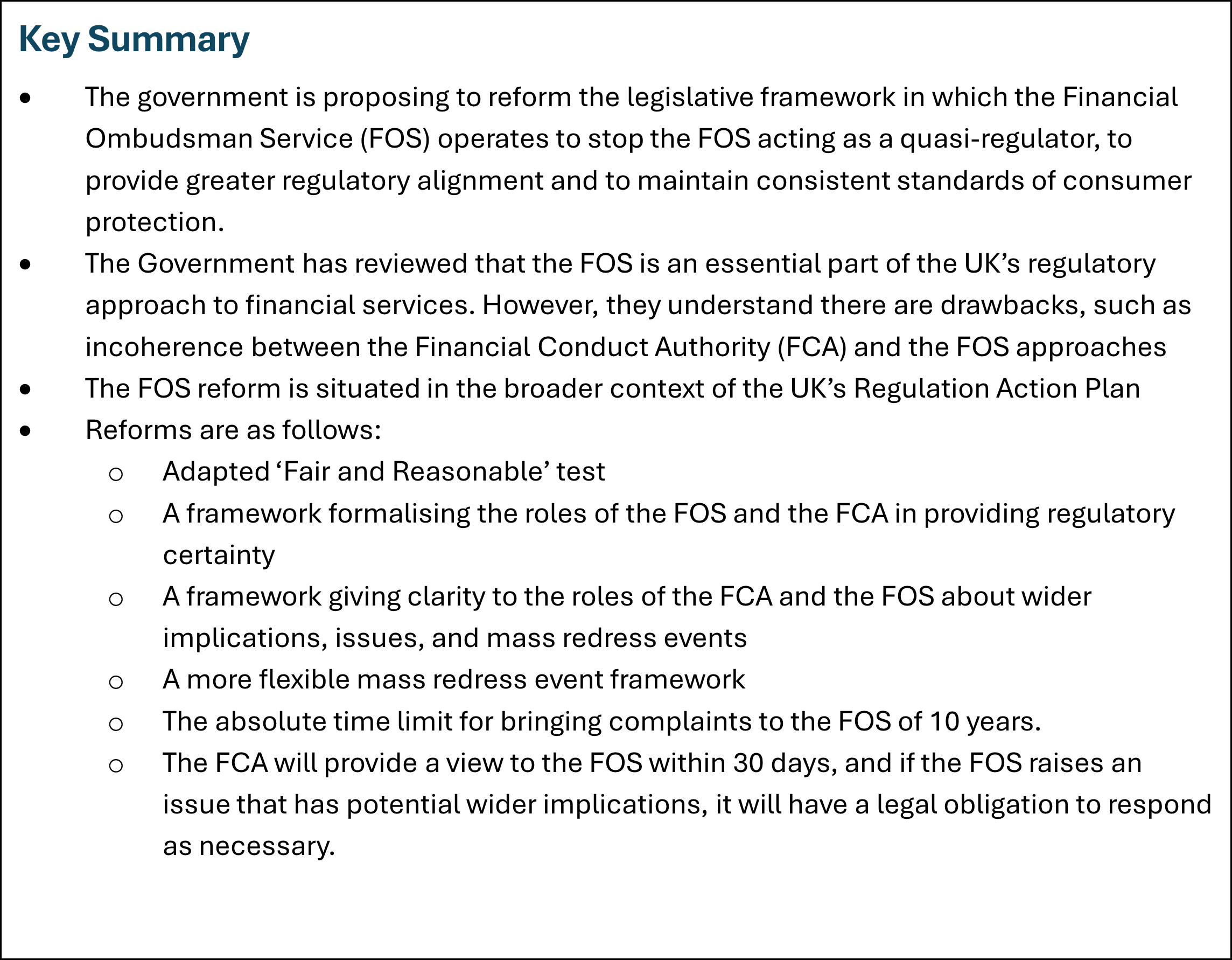

Introduction

HM Treasury’s Review of the Financial Ombudsman Service complements the joint consultation and approaches the review of the Financial Ombudsman Service from a policy and legislative stance. The member briefing should be read in conjunction with the joint FOS/FCA member briefing. ABCUL has included content of the HM Treasury consultation, which has not been covered or slightly differs from that of the FOS/FCA consultation.

Institutional arrangements for the FOS

- The government is seeking views on whether there would be benefits to making the FOS a subsidiary of the FCA, as they acknowledge they work closely already.

- The government has highlighted both the positives and the drawbacks.

- Shared management approaches – which can facilitate better understanding of FCA rules by FOS staff.

- Closer institutional relationship –this could help streamline processes and speed up information sharing.

However,

-

- A potential to compromise operational independence and impartiality

- Implementation challenges – significant time and investment would be needed.

Adapting the Fair and Reasonable Test

- The Government aims to clarify that the fair and reasonable test is what is fair and reasonable for both parties – for the complainant and the respondent.

- The Government will legislate to ensure that if a firm follows FCA rules, it should be treated as acting fairly. The FOS will then need to look at the rules in place at the time and not use newer rules to judge old actions.

- If there are FCA rules or guidance that cover the law, the FOS should use those rules to decide what is reasonable and fair.

- If FCA rules don’t cover the law, the FOS will still have the ability to use the law to decide what is reasonable and fair.

- The law however, may be unclear in some circumstances, and so the FCA , if needed, can ask the courts to make a decision. This is a test case, and after the court has made its decision the FCA will be able to update its rules and guidance to reflect this.

Alternative proceedings

- The FOS used to be able to dismiss a complaint if it thought it was not the appropriate body to deal with the complaint.

- This was stopped by the ADR Regulations, but now the government is planning to remove the FOS from these rules to give it more flexibility again to decide where complaints are best dealt.

Absolute Time Limit

- HM Treasury proposes an absolute time limit in bringing complaints to the FOS of 10 years.

- This absolute time limit, from the date of its implementation, will only apply to all new complaints brought to the FOS. The Complaint must also be submitted within 6 years of the event/issue.

- is more than 6 years have passed, then it can be submitted within 3 years of when the person became aware of the complaint.

- But it should be no later than 10 years since the event occurred.

Role of the Courts

- The Government agrees that some complaints should be handled and are better handled by the courts. The FOS, as a result, will be allowed to dismiss cases and recommend, they go to the courts instead.

- The Government does not support a formal appeal mechanism as it could undermine the FOS’s impartial dispute resolution service.

- It would also put additional pressure on the court system.

Transparency

- The Treasury is concerned that the FOS’s requirement to publish each determination is not the most helpful way in providing a clear view to consumers – over 20,000 decisions are published each year.

- The government is considering requiring the FOS to publish a quarterly thematic guidance document on how particular types of cases are investigated and how FCA standards are applied.

Question 1: Do you agree that, where conduct complained of is in scope of FCA rules, compliance with those rules will mean that the FOS is required to find a firm has acted fairly and reasonably?

Question 2: Will the aligning of the Fair and Reasonable test with FCA rules still allow the FOS to continue to play its relatively quick and simple role resolving complaints between consumers and businesses?

Question 5: Do you agree that there should be a mechanism for the FOS to seek a view from the FCA when it is making an interpretation of what is required by the FCA’s rules?

Question 6: Do you agree that parties to a complaint should have the ability to request that the FOS seeks a view from the FCA on interpretation of FCA rules where the FCA has not previously given a view?

Question 7: Do you agree that parties to a complaint should have the ability to request that the FCA considers whether the issues raised by a case have wider implications for consumers and firms?

Question 8: As part of implementing the proposed referral mechanism, do you think there are any issues which should be considered in order to ensure the mechanism works in the interests of all parties to a complaint?

Question 9: Do you agree that the Chief Ombudsman should have overall authority for determinations made by FOS ombudsmen, and through that authority, should be responsible for ensuring consistent FOS determinations?

Question 10: What approach to transparency arrangements would provide the most accessible way for consumers and firms to understand what outcomes to expect for particular types of cases that the FOS deals with?

Question 12: Taking into account the other reforms proposed in this consultation, do you think that the FOS should be made a subsidiary of the FCA? If so, what are your views on the appropriate institutional arrangements?

Question 13: Do you agree that 10 years is an appropriate absolute time limit for complainants to bring a complaint to the FOS?

Question 14: Do you agree that the FCA should have the ability to make limited exceptions to this time limit?

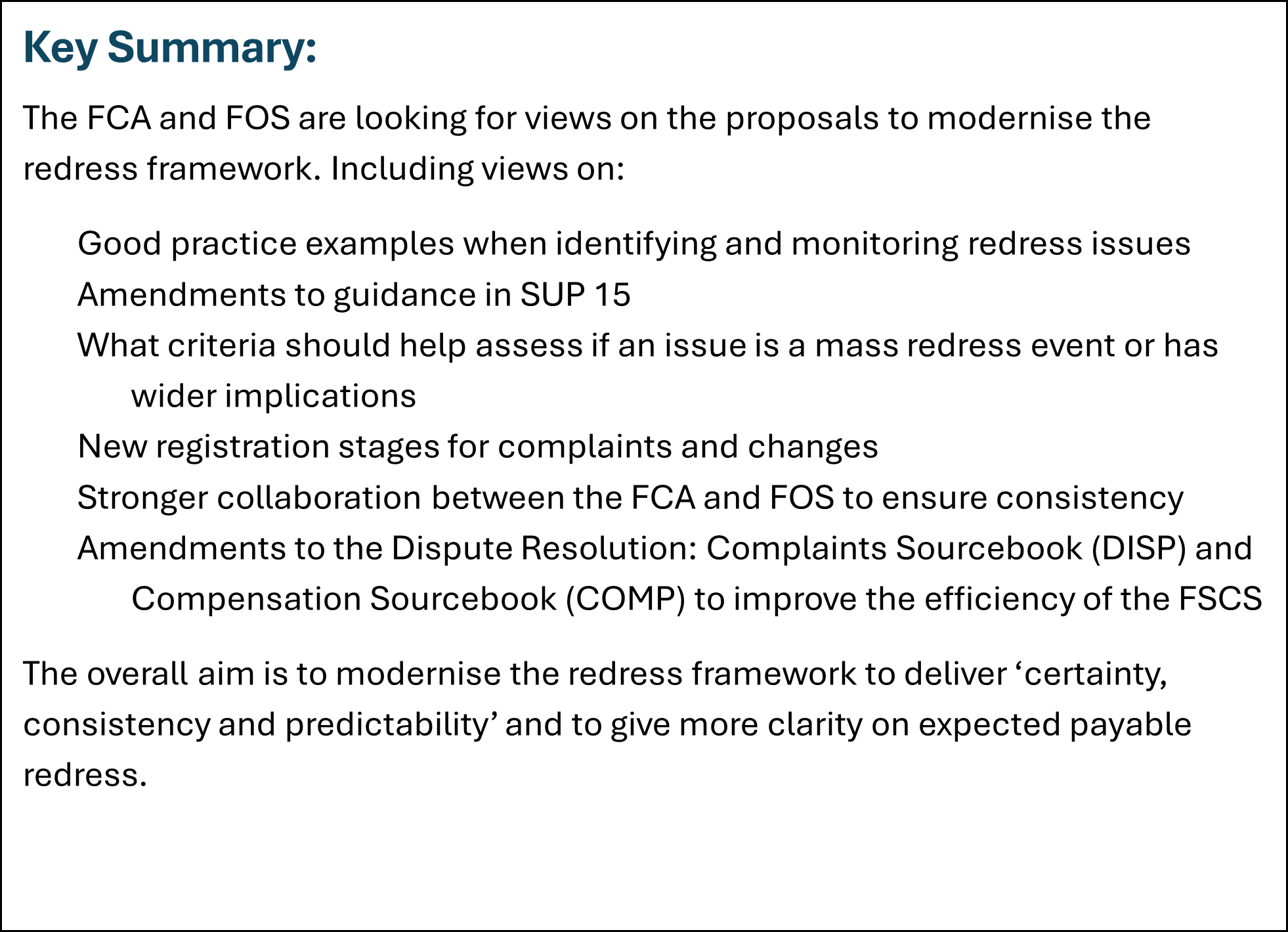

FCA and FOS CP25/22: Modernising the Redress System Members’ Briefing

Introduction

The Financial Conduct Authority (FCA) and Financial Ombudsman Service (FOS) have published a joint consultation: CP25/22 Modernising the Redress System. This briefing highlights the content of the consultation relevant to credit unions and complements the HM Treasury Review of the Financial Ombudsman Service from an operational standpoint, and improving how the FOS functions on a day-to-day basis.

This consultation paper follows the November 2024 joint call for input. The proposals are outlined below:

Improving predictability and consistency (Chapter 2)

- The FOS fair and reasonable test has led to unpredictability, and many are calling the FOS a ‘quasi-regulator’

- The fair and reasonable test is being proposed to remain, but it is aligned more with the FCA’s regulatory standards.

- If an issue needs regulatory interpretation, the FOS will consult the FCA

- Where FCA rules are material to the complaint – if a firm is complying with the FCA rules with the FCA’s intended purpose, then the FOS cannot hold a firm to a different standard – this will allow for better legal clarity.

- If rules are not material or outside the scope of FCA rules, the FOS still apply its ‘fair and reasonable’ test.

Formal Referral Mechanism

- Treasury is proposing to introduce a formal referral mechanism between the FOS and the FCA – this would mean that the FOSD would be able to refer issues that need interpretation to the FCA to reach a fair outcome.

- This referral process with be built on the current Memorandum of Understanding (MoU).

- It aims to formalise the referral process into a more structured route

- Where the FOS has requested a view from the FCA, a 30-day deadline for the FCA to respond is proposed.

- This referral process aims to ensure that both the FCA and the FOS will consult with each other from an early stage and communicate appropriately.

Right to Referral

- Firms and complainants should be able to ask that the FOS refer an issue to the FCA – this would be allowed after the initial assessment but before final determination.

- It isn’t, however, meant to act as an appeals process – but to allow a challenge to regulatory interpretation.

Transparency around decisions

- The FOS is legally required to publish each decision. The treasury is reviewing to see if this is still a helpful way due to the large volumes of complaints being brought to the FOS.

- Considerations are being put forward for the FOS to publish a quarterly ‘lessons learned’ document.

Time Limits

- The Treasury is looking to introduce a 10-year longstop date for complaints as well as giving the FCA flexibility with exceptions.

Improved outcomes for mass redress events (Chapter 3)

Challenges

- Mass redress events and increases in complaint numbers can overwhelm systems and processes, causing delays.

- Professional Representatives have been a cause for concern as firms have highlighted that they sometimes put forward meritless complaints.

- The FCA and FOS recognise these challenges , but recognise the value that PRs have in the redress system.

Defining Mass Redress Events

- The FCA and FOS propose to consider Mass Redress Events (MREs) against a 6-criterion framework.

- Proposed criteria are:

- Affects a high number of consumers.

- Has a significant impact on individual consumers, including those in vulnerable circumstances.

- It is likely to lead to a high redress bill.

- Results in a significant number of firms being unable to meet their redress liabilities.

- Leads to a high number of Financial Ombudsman complaints.

- Driven by a systemic/repeatable failing that damages confidence in the financial system

Managing a mass redress event

- Proposals to allow the FOS to use a firm’s redress scheme to settle complaints

- allow the FCA to direct the FOS to refer cases back to firms so they can sort it out directly

- Allow more flexibility for the FCA to start a consumer redress scheme

Firms identifying, reporting and rectifying harm effectively (Chapter 4)

Guidance for firms in Dispute Resolution: Complaints Sourcebook (DISP)

- The FCA are considering options to simplify the DISP rules affected by PRIN 2A.2.5R and PRIN 2A.10

PRIN 2A.2.5R is the rule that firms must avoid causing foreseeable harm, and PRIN 2A.10 explains what firms need to do if they discover they have caused harm.

- Further guidance has been set out in Annex 4, page 74, which highlights good and poor practices.

Opportunity for firms to resolve complaints fairly

- Extension of the 8-week deadline as set out in DISP is not seen as appropriate, as it is generally seen to work well.

- However, additional proposals have been put forward to give the FCA more flexible powers to pause the DISP timescale as part of Mass Redress Events (MRE) tools.

- There is no plan for the reintroduction of the 2-stage procedure, and instead, more clarity will be given to firms through the new referral mechanism and guidance where needed.

- Steps will also be taken to better manage and identify potential systemic issues.

Collecting data

- Consultation is ongoing on changes to the complaints reporting rules, and if implemented, would mean firms report complaints on a 6-monthly basis.

- In addition to SUP 15, clarificatory guidance is proposed in SUP15.3.8G, which highlights situations where it is expected that firms notify the FCA.

- This proposed guidance includes criteria and thresholds for when firms should submit a SUP 15 notification

- Proposed criteria are:

-

- Affects a high number of consumers (>40% of the firm’s consumers from the affected product line or service), or

- Has a high potential redress bill; should complaints be upheld by the firm, the Financial Ombudsman or the courts (>£10m or 50% of the firm’s annual revenue from the affected product or service line), or

- Has led to a significant spike in consumer complaints, or

- Leads to concerns that redress that could be due if the complaints were upheld, either via the firm, the Financial Ombudsman or the courts, may adversely affect the firm’s capital adequacy or solvency, or

- Affects multiple consumers and has a significant impact on each individual consumer (>£10k loss per consumer on average).

Financial Ombudsman activities and complaint procedures (Chapter 5)

- Treasury is proposing changes to the statutory framework of the FOS – they want formal authority for all decisions to be made by the Chief Ombudsman, who can also delegate this function to their team, with limitations.

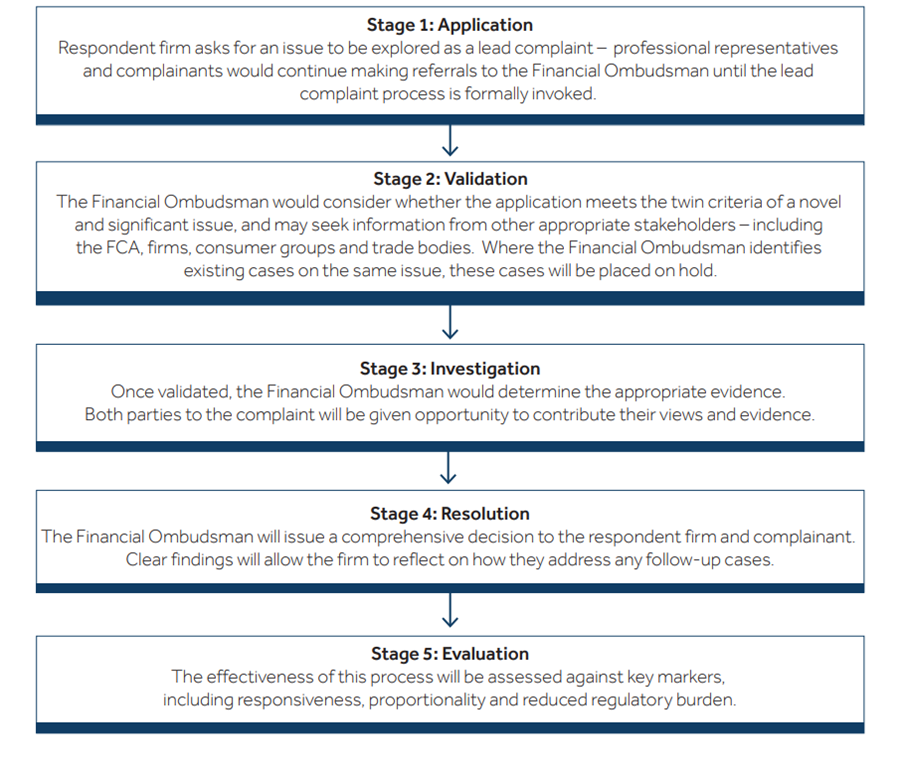

FOS ‘Lead Complaints’ process

- The FOS is proposing to introduce a structured ‘lead complaints’ process to address new and significant complaint issues.

A lead complaint is a case that is chosen by the FOS, which raises a new or significant issue, likely to affect other complaints

- The structure is proposed as follows:

Case fee rules and rules for complaints brought by Professional Representatives (PRs)

- The FOS is proposing to introduce a registration stage to assess whether the complaint is appropriate to take it to the investigation stage.

A registration stage is a new step that is being proposed by the FOS when handling complaints, it will be before the complaint is investigated and charged a full case fee. It will allow the FOS to pre-screen complaints before a full investigation.

- Before a complaint can be registered, it has to fit certain criteria, including:

- Final Response Letter (FRL): The respondent firm must have issued a FRL, or the 8-week deadline for providing a final response to a complaint under DISP 1 must have passed.

- No Fundamental Challenges: There must be no fundamental objections to the complaint’s admissibility or jurisdiction.

- Minimum Evidential Standards: The complaint must meet minimum evidential standards, which may be tailored to specific products or policy areas to ensure they are relevant and proportionate

- In introducing this registration stage, rules that might be affected are:

- DISP 1: To include this registration stage and the required evidence

- DISP 3.5: Defining when a case becomes chargeable

- FEES 5: To support flexible fee levels.

- DISP 3.3: Allow for dismissal if a redress scheme is available

Other changes to improve Financial Ombudsman and FSCS operational efficiency (Chapter 6)

DISP (Dispute Resolution) Changes

DISP 1.4.4AG – Clarified Cooperation Rules

- Firms will need to fully cooperate with the FOS to comply with directions on evidence and information.

DISP 1.6.1R – Complaint Acknowledgement

- Firms will need to let customers/members know how long they will have to wait for a final response – premature referrals to the FOS cause delays and are burdensome for the Financial Ombudsman.

COMP (Compensation) Changes – FSCS

(COMP 4 &12A) Eligibility rules – Making it clearer who can and can’t claim compensation

(COMP 6) Default Rules – Broaden the scope of the FSCS to be able to declare a default

(COMP 11) Flexibility of Payment Rules – the FSCS will be able to have greater flexibility on where compensation is paid

(COMP 12) Discretion to Settle – the FSCS will be able to use its discretion to settle without further investigation.

Question 1: Do you agree with the proposed criteria for considering whether an issue is a mass redress event?

Question 2: Do you agree with the guidance provided in Annex 4 of this consultation paper, for how firms can proactively identify and rectify potential issues?

Question 3: Do you agree with the additional guidance proposed at SUP 15.3.8G for when firms are expected to report serious redress risks or issues to the FCA?

Question 4: Do you support the introduction of a ‘lead complaints’ process to address novel and significant complaint issues?

Question 5: Do you think that the lead complaints process will achieve its intended benefits?

Question 6: Do you agree that firms should be allowed to pause related complaints while lead cases are under investigation in the lead complaints test process?

Question 7: What safeguards should there be to ensure the lead complaints process is not used to delay or avoid complaint resolution?

Question 8: Do you agree in principle with the introduction of a new registration stage before a complaint is investigated by the Financial Ombudsman?

Question 9: Do you agree that the registration stage will help complainants preparing and submitting complaints to the Financial Ombudsman?

Question 10: What safeguards should there be to ensure the registration stage does not limit access to justice, particularly for vulnerable consumers?

Question 11: Do you agree that the Financial Ombudsman being able to pause or pass back cases at the new registration stage would improve respondent firms’ ability to manage mass redress events or emerging regulatory issues?

Question 12: Do you agree that the Financial Ombudsman should consider differential case fees for cases in the registration stage?

Question 13: Do you agree with the proposed changes to DISP to improve the Financial Ombudsman’s operational efficiency?

Question 14: Do you agree with the proposed amendments to COMP 4 and COMP 12A to simplify the list setting out who is and is not eligible to make a claim to the FSCS?

Question 15: Do you agree with the proposed amendments to COMP 6.3.4R to enable the FSCS to determine a relevant person in default, where they are not co-operating with the FSCS, or where personal circumstances prevent them from co-operating?

Question 16: Do you agree with the proposed amendments to COMP 11.2 to give the FSCS greater discretion over where compensation is paid under specific circumstances as described in that provision?

Question 17: Do you agree with the proposed amendments to COMP 12.2.10R and the additional factors listed in COMP 12.2.11R that FSCS must take into account, when considering if a claimant is eligible?

Question 18: Do you agree with our assumptions about the sizes of the compliance and legal teams involved in familiarisation and gap analysis, and with our treatment of costs associated with changes to firms’ complaint acknowledgement letters?

Question 19: Do you agree with our analysis of the costs and benefits of these proposals?

Both consultations close on 8 October 2025

ABCUL is eager to hear our member credit unions’ views on the proposals and asks that all responses be sent to advocacy@abcul.org and received by the close of business on Monday, 4 October 2025.